The Dividend Kings are well known stocks for dividend growth investors. They are a group of U.S. stocks that have raised the dividend for 50+ years. This is no small feat as there are only 36 companies on this list as of the latest update. This is out of over 6,000 companies listed on U.S. stock exchanges. For further perspective, these companies have consistently raised the dividend through multiple recessions, market crashes, wars, and so on. So, the bottom line is that the Dividend Kings are an exclusive list.

However, some of the Dividend Kings are extremely well-known. Most dividend growth investors know that companies like Coca-Cola (KO), Johnson & Johnson (JNJ), 3M Company (MMM), Proctor & Gamble (PG), and Altria Group (MO) are Dividend Kings. But there are companies that are not as well-known too but equally as successful at raising the dividend for 50+ years. In this article, I cover 3 Lesser Known Dividend Kings: Universal (UVV), SJW Group (SJW), and Northwest Natural Holdings (NWN).

Note: This is a guest post by Dividend Power. Continue enjoying the read!

Universal

Universal is one of the smaller Dividend Kings with a market capitalization of only about $1.27 billion. The company also has one of the higher yields of the Dividend Kings at roughly 6.0% as of this writing. This could be because Universal’s growth prospects are not too robust, and the stock price has traded within a range for many years. Universal is the global leader in supplying tobacco leaf and this is a declining business. But it is a profitable one and further it is a mature industry with entrenched relationships. This provides some defensibility and a moat. Total revenue was $1,983 million in fiscal 2020.

Universal was founded in 1918. The company buys, processes, stores, packages, and sells tobacco leaf to manufacturers for tobacco products. This includes flue-cured, burley, oriental, and dark leaf tobaccos. Universal operates globally in 30 countries. The company handles about 25% – 35% of African tobacco, 15% – 25% of Brazilian tobacco, and 35% – 45% of U.S. tobacco. Universal is in effect an intermediary between tobacco farmers and manufacturers.

The company has recognized that they are in a declining business and has made acquisitions in fruits and vegetables processing companies. Universal acquired FruitSmart and Silva International in 2020. This is a fragmented market and Universal has room to grow organically and by acquisition.

Universal’s dividend is currently safe despite the high yield and low growth, but dividend safety is declining.

The payout ratio is about 88% so it is above my target of 65%. The company raised the dividend ~36% in fiscal 2019 and this was followed by small increases. However, the payout ratio rose from roughly 50% to about 68% and has trended higher since then. The company generated ~$220 million in operating cash flow in the LTM and capital expenditures were only $66 million. This means that Universal has more than enough FCF to meet the $75 million needed to pay the dividend.

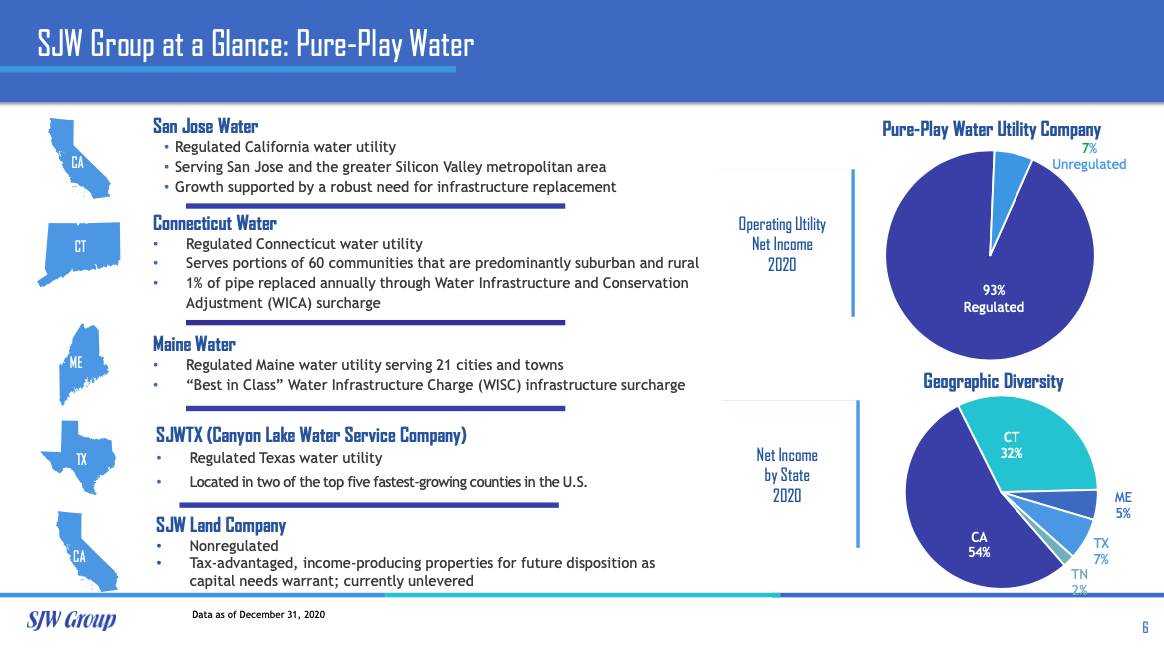

SJW Group

SJW Group is the next lesser known Dividend King. The company is a regulated water utility that serves over 1 million people in areas around Silicon Valley including Santa Clara, San Jose, Cupertino, Las Gatos, and other areas. The utility also has operations between San Antonio and Austin. SJW Group acquired Connecticut Water Service for $1.1 billion in 2019 and now serves nearly 500,000 customers in Connecticut and Maine. Interestingly Connecticut Water Service was a Dividend King before being acquired and the deal represented a Dividend King buying a Dividend King, which as a rare occurrence. Total revenue was about $565 million in 2020 and the current market capitalization is only about $2.1 billion.

SJW has raised the dividend for 54 consecutive years and has paid a dividend for 77 consecutive years. The utility most recently increased the dividend by 6.3% in March 2021. The company has a raised the dividend at a 4.8% CAGR in the trailing 10-years and a faster 10.9% CAGR in the trailing 5-years. The current dividend is $1.36 per share and the dividend yield is 1.97%.

SJW’s dividend is safe as well.

The current payout ratio roughly 70%, which is higher than my threshold of 65%. But regulated water utilities have predictable earnings making a slightly higher payout ratio acceptable. The dividend is also safe from the perspective of cash flow. SJW Group had operating cash flow of $104 million. The utility spent $195 million on capital expenditures, but most utilities cover capital expenditures from debt. The dividend required approximately $37 million indicating that operating cash flow covered the dividend by over 2X.

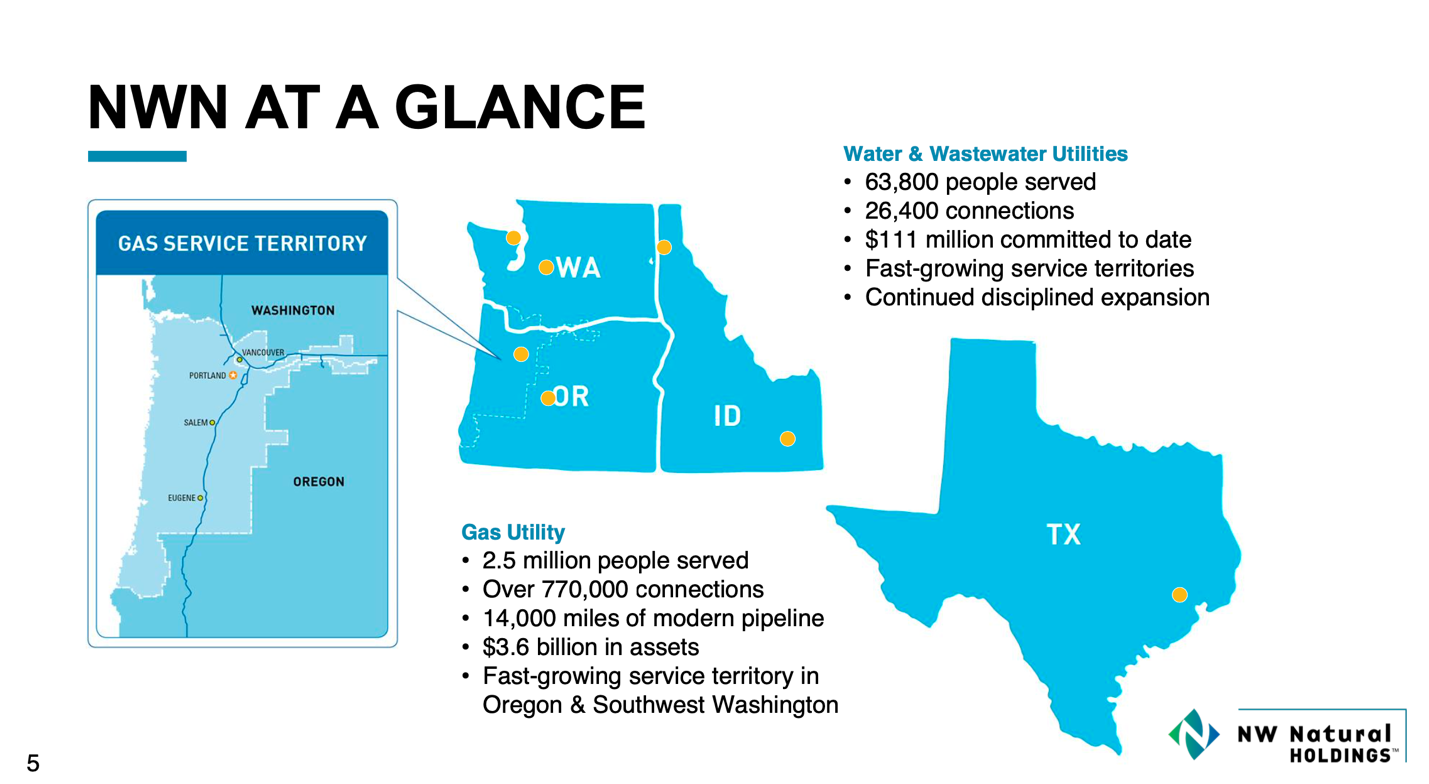

Northwest Natural Holdings

The third lesser known Dividend King that I discuss is Northwest Natural Holdings. The company is another regulated utility but this one is a natural gas utility that traces its founding back to 1859. Northwest Natural serves approximately 2.5 million residential, industrial, and commercial natural gas customers in Oregon and Southwest Washington. The utility has also expanded into regulated water and wastewater operations and serves 63,800 customers in Washington, Oregon, Idaho, and Texas. Total revenue was about $774 million in 2020 and the current market capitalization is only about $1.6 billion.

In addition to being a Dividend King, Northwest Natural is one of the few companies to have raised the dividend for over 60 years. In fact, the utility has raised the dividend for 65 years. There are only three companies that have raised the dividend for 65+ years on U.S. stock exchanges. The current yield is 3.67%.

The utility’s dividend growth rate has been low though at only 1.3% CAGR in the past decade and 0.53% CAGR in the trailing 5-years. This is in part due to a higher payout ratio and a focus on acquisitions in the water and wastewater regulated utility market.

That being said, Northwest Natural’s dividend is safe.

The payout ratio is approximately 76%, which is acceptable for a regulated natural gas and water utility due to more predictable earnings. The dividend is also safe from the perspective of cash flow. Northwest Natural has operating cash flow of about $175 million in 2020. The dividend required only $55 million meaning that it was covered by ~3X by operating cash flow. Debt is not too much of a concern either. Northwest Natural has an AA-/stable credit rating from S&P Global and A-2/stable credit rating from Moody’s. These mean high quality, very strong capacity to meet financial commitments.

Final Thoughts on 3 Lesser Known Dividend Kings

I like the Dividend Kings because of their consistency in raising the dividend. Furthermore, once a stock makes it to this list it is rare that it drops off except by acquisition or merger. Dividends matter to investors because they represent a return to shareholders and further can be a major part of total return. The three stocks discussed above are solid companies and will likely continue raising the dividend in the foreseeable future.

Disclosure: None

Author Bio: Dividend Power is a self-taught investor and blogger on dividend growth stocks and financial independence. Some of his writings can be found on Seeking Alpha, TalkMarkets, ValueWalk, The Money Show, Forbes, Yahoo Finance, and leading financial blogs. He also works as a part-time freelance equity analyst with a leading newsletter on dividend stocks. He was recently in the top 4% out of over 8,091 financial bloggers as tracked by TipRanks (an independent analyst tracking site) for his articles on Seeking Alpha.

Disclaimer: Dividend Power is not a licensed or registered investment adviser or broker/dealer. He is not providing you with individual investment advice. Please consult with a licensed investment professional before you invest your money.